How the US, UK, and UAE Actually Tax Gold-Backed Tokens

Gold had one of its strongest runs on record heading into 2026, and a growing share of that demand is flowing through tokenized gold rather than bars or coins. Platforms now let investors buy fractional, gram-denominated ownership of vaulted gold and hold it in a crypto wallet instead of a safe. The problem is that almost nobody selling tokenized gold explains how the gains are actually taxed, and the honest answer is that tax authorities have not fully caught up either. This guide breaks down what the IRS, HMRC, and the UAE's Federal Tax Authority currently say, where the rules are genuinely unsettled, and how real investors, including people living in one country while holding tokens issued in another should think about filing in 2026.

Disclaimer

This guide above is for general educational purposes only and does not constitute tax, legal, or financial advice. Tax treatment of tokenized gold depends on your specific residency, citizenship, holding structure, and the terms of the platform issuing the token, and rules referenced here (IRS, HMRC, VARA, and CARF guidance) can change without notice.

Always confirm your position with a licensed tax advisor or accountant in your jurisdiction before making a buy, sell, swap, redemption, or gifting decision.

Are You Taxed as a Gold Investor or a Crypto Investor?

Before going on to talk about tax in detail, it’s not bad to have a quick review of how to buy tokenized gold online. Most articles on this topic pick one lane, either the crypto tax rules or the precious metals rules, and never address the actual point of confusion: tokenized gold sits between two established tax regimes that were never designed for each other, and no major tax authority has published a rule written specifically for gram-backed digital gold.

Physical gold bars and coins are classified in the United States as collectibles under Internal Revenue Code Section 408(m), capping long-term gains at 28% instead of the usual 15-20% capital gains tax bands. Cryptocurrency, by contrast, is treated as property under Notice 2014-21 and taxed at ordinary short-term or preferential long-term capital gains rates, with no collectibles surcharge. A gold-backed token is legally a digital asset, but economically represents an allocated bar in a vault, the same look-through question the IRS has only addressed for NFTs, ruling that NFTs representing collectibles can inherit collectible treatment depending on what the token represents.

No IRS ruling currently classifies tokenized gold as subject to the 28% collectibles tax bracket, so most platforms and tax software default to the standard digital asset capital gains treatment. Investors who redeem tokens for physical bars rather than cash are on shakier ground, since that redemption arguably converts a digital asset into a collectible at the moment of exchange, the single biggest unresolved question in tokenized gold tax planning heading into 2026, worth confirming in writing with a CPA rather than assuming either answer.

The United Kingdom sidesteps this ambiguity differently. HMRC does not have a separate collectibles regime for individuals at all; it taxes based on the substance of the transaction, not the label of the asset. Its cryptoassets manual states that where a token represents an underlying asset such as a gold bar, the token's location for Capital Gains Tax purposes follows the location of that gold bar, not the location of the blockchain or the investor. That is a meaningfully different legal test than anything in US or UAE guidance, and it matters most for non-UK residents and remittance-basis taxpayers.

The UAE avoids the debate entirely for individuals: with no personal capital gains tax on any asset class, the collectible-versus-crypto distinction that dominates US and UK planning is simply irrelevant to a private investor holding tokenized gold in Dubai or Abu Dhabi.

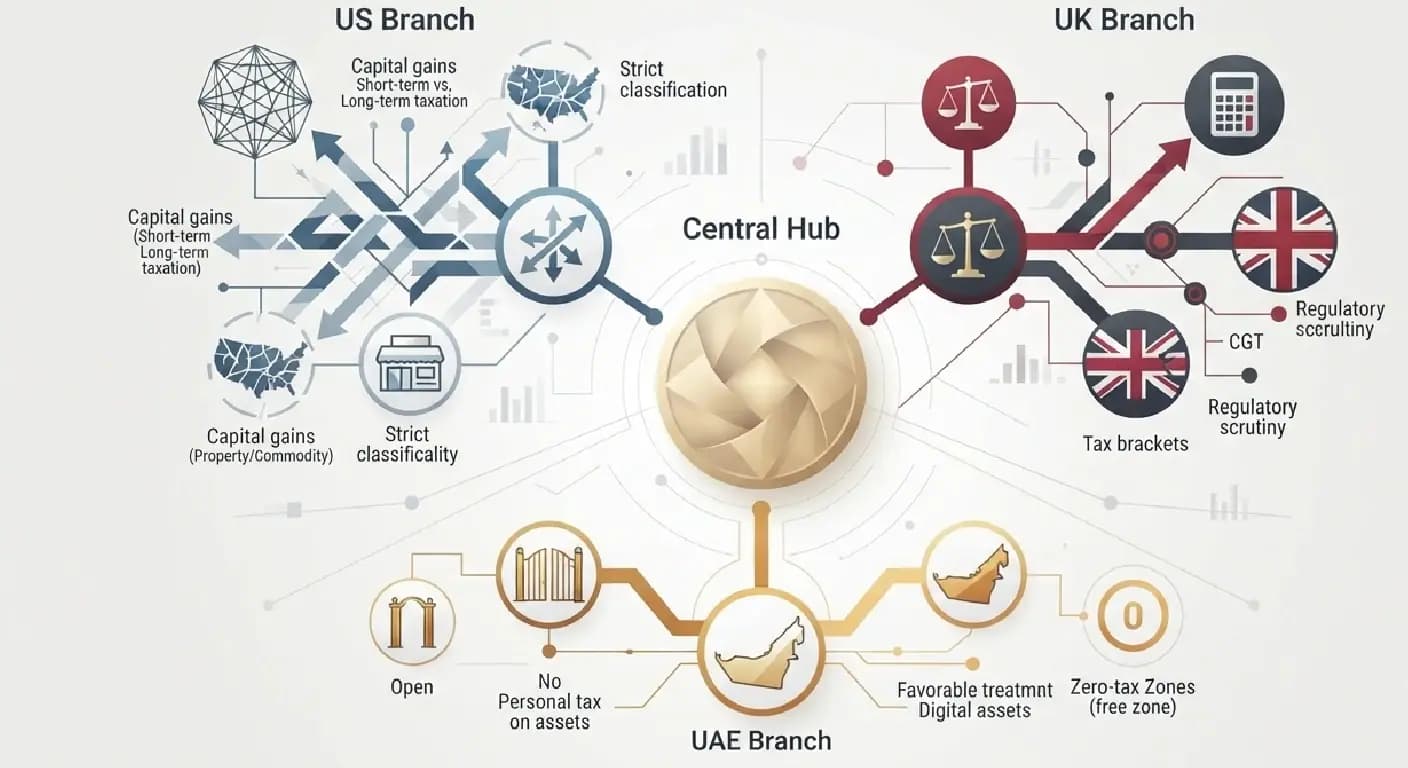

Country-by-Country Comparison at a Glance

| United States | United Kingdom | United Arab Emirates | |

|---|---|---|---|

| Tax authority | IRS | HMRC | FTA / VARA |

| Individual capital gains tax | 0-20% (property) or up to 28% if treated as a collectible | 18% or 24% (Capital Gains Tax band-dependent) | 0% no personal capital gains tax |

| Tax-free allowance | None (all gains reportable) | £3,000 annual exempt amount | Not applicable |

| Legal classification | Digital asset / property (crypto framework); collectible status untested for gold tokens | Cryptoasset; taxed on substance, situs follows the underlying gold | Virtual asset under VARA; not a taxable event for individuals |

| Reporting form | Form 8949 + Schedule D | SA108 (Self Assessment, cryptoassets section) | None for individuals; Corporate Tax return if run as a business |

| 2026 reporting shift | Form 1099-DA broker reporting expands | CARF data-sharing begins January 2026 | CARF exchange reporting phasing in from 2027-2028 |

United States: Digital Asset Rules, With a Collectibles Asterisk

For US tax purposes, the IRS treats all digital assets, including gold-backed tokens like PAXG, as property under Notice 2014-21. That means buying tokenized gold with US dollars is not a taxable event, but selling, swapping, or spending it is. Gains held one year or less are taxed as ordinary income (up to 37%), while gains held longer than a year qualify for the standard long-term capital gains tax rates of 0%, 15%, or 20%, reported on Form 8949 and Schedule D.

Where it gets complicated is redemption. Several tokenized gold issuers allow holders to redeem tokens for physical bullion above a minimum threshold. The moment you take physical delivery, you are arguably converting a digital asset into a collectible, and any future sale of that physical bar would fall under the 28% collectibles rate that applies to traditional gold. Tax advisors are split on whether the original token gain itself should also be recharacterized at redemption, so documenting the fair market value at redemption is essential regardless of which position you take.

- Wash sale rules do not currently apply to crypto-classified assets, including tokenized gold, so you can sell at a loss and immediately repurchase without the 30-day restriction that applies to stocks.

- High earners should factor in the 3.8% Net Investment Income Tax (NIIT) on top of the capital gains rate if modified adjusted gross income exceeds the relevant threshold.

- Gifting tokenized gold up to $19,000 per recipient in 2026 avoids gift tax reporting, and the recipient inherits your original cost basis and holding period.

- Tokenized gold held inside a self-directed IRA has not been addressed by IRS guidance the way physical bullion IRAs have (IRC Section 408(m)(3)); most custodians currently treat digital asset tokens, gold-backed or not, as outside the approved-metals exception.

United Kingdom: Capital Gains Tax, Situs Rules, and CARF Reporting

HMRC does not run a bespoke tokenized gold regime. It applies its existing cryptoassets framework, taxing individual holders under Capital Gains Tax rather than Income Tax in almost all cases, since HMRC's default assumption is that most people investing in cryptoassets are investors, not traders. Gains are calculated using the Section 104 pool method, which blends the cost of every purchase of the same token into a single average cost basis, then applies same-day and 30-day matching rules before falling back to the pool.

For the 2026 tax year, individuals pay Capital Gains Tax at 18% or 24%, depending on their income tax band, after applying the £3,000 annual exempt amount, which applies to all capital gains, not just crypto. Every disposal selling for GBP, swapping into another token, or spending tokenized gold on goods and services counts as a taxable event and must be reported via the dedicated cryptoassets section on Self Assessment form SA108, due by 31 January following the tax year.

The situs rule is the detail most guides miss: because a gold-backed token represents a specific allocated bar, HMRC treats the token as located wherever that bar is physically vaulted, unlike a pure cryptocurrency with no underlying asset. For remittance-basis and non-domiciled taxpayers, this can materially change what counts as a UK-source gain versus a foreign-source gain.

- From January 2026, the Cryptoasset Reporting Framework (CARF) requires UK platforms to report user transactions directly to HMRC, and that data will be exchanged internationally, so undeclared gains are far easier for HMRC to trace than in prior years.

- Transferring tokenized gold between your own wallets is not a disposal; transferring it to anyone other than a spouse or civil partner is.

- Losses can be carried forward and offset against future gains, or claimed up to four years after the end of the relevant tax year.

United Arab Emirates: Zero Personal Tax, With Conditions

The UAE remains the simplest jurisdiction in this comparison for an individual investor. There is no personal income tax and no capital gains tax on any asset class, tokenized gold included, whether you buy, hold, trade, or redeem it for physical bullion. Virtual asset activity is regulated for consumer protection and anti-money-laundering purposes by the Virtual Assets Regulatory Authority (VARA) in Dubai and the Financial Services Regulatory Authority in Abu Dhabi Global Market, but neither regulator imposes tax on individual gains.

That zero-tax outcome only applies once you are genuinely a UAE tax resident, generally established by spending 183 or more days in the country and holding a valid residency permit. Simply opening an account with a UAE-licensed platform while living elsewhere does not transfer any tax benefit to you. The exemption also has a business-activity ceiling: individual crypto or tokenized-gold activity that resembles a trading business and exceeds roughly AED 1,000,000 in annual revenue can trigger UAE Corporate Tax registration even without forming a company, and any company-level trading or tokenization business pays the standard 9% Corporate Tax above the AED 375,000 profit threshold.

- US citizens and green card holders remain taxable on worldwide income regardless of UAE residency, because the United States taxes based on citizenship, not physical location.

- VAT on core crypto and tokenized-asset transactions has been exempt since a 2024 Cabinet Decision, though ancillary business services may still be subject to the standard 5% VAT.

- CARF reporting by UAE-based exchanges is expected to phase in from 2027-2028, meaning the current lack of automatic data-sharing will not last indefinitely.

After all the above data, maybe you are interested in investing in gold in the UAE. Here is more info on how to buy digital gold in the UAE.

Cross-Border Scenarios People Actually Search For

Most guides miss the important point that actually drives most questions on this topic because most tokenized gold investors do not fit neatly into a single jurisdiction.

- A US citizen living in Dubai: the UAE imposes no local tax, but citizenship-based taxation means every disposal must still be reported on Form 8949, exactly as if you lived in the US.

- A UK resident holding a token vaulted outside the UK: the situs rule may treat part of the gain as foreign-source for remittance-basis taxpayers, but does not remove CGT liability for UK-domiciled residents.

- A digital nomad with no fixed residency: liability follows days present and center-of-life factors, not where the exchange is incorporated, so a platform's "tax-free" marketing describes its own jurisdiction, not yours.

- An investor redeeming tokens for physical delivery: this single transaction shifts the tax analysis in every jurisdiction here, since it converts a digital asset into physical bullion.

Mistakes Investors Commonly Make

- Assuming a platform's marketing claim of being "tax-free" refers to its users' personal tax liability rather than the platform's home jurisdiction.

- Treating a crypto-to-crypto swap between two gold tokens as a non-event because no fiat currency changed hands.

- Forgetting that moving to a zero-tax jurisdiction does not end tax obligations for US citizens or for UK non-doms with UK-source gains.

- Failing to keep fair-market-value records at the exact moment of any redemption for physical bullion, which is the single most disputed valuation point across all three jurisdictions.

The Bottom Line

Tokenized gold is not a tax-free method of getting ownership of physical gold; neither is it automatically subject to the 28% collectibles tax that is applicable to bars and coins. In fact, the accurate response for 2026 is that the US and UK are tentative on the answer; the UAE has finalized the answer for personal ownership: nada, and the single transaction that would alter all of that is swapping your token for physical gold. The following is for general information only and does not constitute tax, legal, or financial advice tax rules will vary based on individual circumstances like residency and Citizenship, so consult with a tax professional to determine how this may impact your personal situation.

Sources

- IRS Digital Assets

- IRS Investments in Collectibles in Individually Directed Qualified Plan Accounts

- Deloitte TaxScape HMRC Approach to Taxation of Cryptoassets

- BDO New Rules in 2026 Will Make It Harder for Crypto Investors to Evade Tax (CARF)

- LearnSignal HMRC Cryptoassets: UK Tax Treatment for Practitioners, 2026 Guide

- Blockpit Crypto Tax United Kingdom (HMRC)

- Tulpar Tax Cryptocurrency Taxation in UAE, 2026

- CCN 0% Crypto Tax in 2026: UAE, Cayman, Bermuda, Plus Conditional Regimes

- IMI Daily 20 Livable Countries That Don't Tax Crypto Gains in 2026

- WealthManagement.com Precious Metals Tax Rules Advisors Must Know in 2026

- Accounting Today Beware of Tax Implications of Selling Precious Metal

- Koinly Crypto Taxes: Expert Guide 2026 (NFT collectibles look-through)

- WEEX Crypto Wiki PAX Gold vs Physical Gold: Which Is Better for Investors?

Toofan Shaterloo

Toofan ShaterlooBuilding tokenised gold infrastructure for a multipolar world. Board: @HectocornGroup. Prev: Netcore, Dengage. Operator → $300M–$1B. 1x exit. Top 100 UK Tech Influencer. Gold is the hedge.

Related posts

All posts

Toofan ShaterlooMay 28, 2026

How to Invest in Gold?

Investing in gold in 2026 offers diverse methods to hedge against inflation and protect wealth, ranging from traditional physical bars to modern, liquid tokenized gold and ETFs. Because gold provides stability rather than high growth, it is best used as a portfolio diversifier, typically 5% to 15% of your total assets, to reduce risk during economic uncertainty. Choosing the right method depends on your budget and custody preferences, but always prioritize regulated platforms with audited, transparent gold reserves to ensure security.

Toofan ShaterlooJun 1, 2026

Digital Gold Investment Guide

Tokenized gold is a major new development in gold investment since the launch of ETFs in 2003. It allows people to own physical gold through blockchain technology, enabling quick transactions and around-the-clock access. Unlike traditional paper claims, tokenized gold offers clear proof of reserves, providing trustworthy information. This makes it an important tool for modern investors dealing with current global and currency uncertainties.

Toofan ShaterlooJun 3, 2026

What Is Tokenized Gold?

Quick answer: Tokenized gold is a digital token on a blockchain that gives you direct legal ownership of physical gold sitting in a professional vault. When you buy one token, you own a specific, weighed quantity of real metal, not a share in a fund, not a futures contract, not a promise. The token is your proof of ownership. It lives in your wallet, trades around the clock, and can be redeemed for the actual gold if you ever want it.